Yesterday’s Fed rate hike to 100-125 basis points came with a surprisingly, hawkish statement. Many market participants are surprised at the statement especially with the poor CPI inflation reading that came out in the morning. With recent economic data not meeting expectations, many fear that the Fed may be on a path of hiking rates too quickly. Subdued wage inflation and a flat yield curve also weigh into investors fears. Contrary to the recent data, Fed Chair Yellen still believes wage inflation should pick up. She believes with a tight labor market, it is only a matter of time before it picks up. With the Fed’s revised long-term unemployment being reduced one basis, she argues that the unemployment rate will continue to drop and this will lead to wage inflation. This thinking shows her belief in the modern Phillips Curve.

FedWatch Tool by the CME Group shows low probability for a rate hike to 125-150 basis points

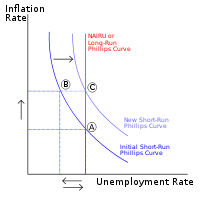

According to the Phillips Curve, inflation and unemployment are inversely related in the short term, but not in the long run. In the long run, unemployment is said to go back to the natural rate of unemployment. Although, in recent years there has been a lot of controversy surrounding the Phillips curve, but many still believe it to hold true. Essentially once slack is removed from the economy, wage inflation will increase. The unemployment rate printing lower than the natural rate of unemployment is a good indicator of removed slack. That is precisely where we are in the economy right now.

Modern Phillips Curve

The logic of the Phillips Curve is quite simple, when there are fewer available workers, you must pay them higher to obtain them. This is the Yellen’s argument to keep the Fed on a monetary tightening route. The fact that the unemployment rate ticked lower to 4.3% on the most recent reading, shows that there still is a little bit of slack in the economy. So there is not to be any need to worry yet since we are still seeing the labor market remove the little slack there is left. If we enter an instance when there is no change in unemployment or the unemployment rate ticks up with no wage growth, then there would be cause to worry.

Wage growth after the 2001 recession accelerated once unemployment crossed below the natural rate of unemployment

With all that said, there is still fear that we will not see rising inflation or wage growth and that the Fed is hiking rates too quickly. Historical precedent can shed some light for us. In 2001 after the recession following the tech bubble, we were in a period of subdued wage inflation. Only once the unemployment rate crossed below the natural rate of unemployment did we start seeing wage growth. During this time before the wage growth the Fed at the time were increasing interest rates. The fed tightening at the time did not subdue wage growth or inflation. Although, after the 01’ recession inflation and wage growth came back faster than this past one, we have to note the remarkable differences between the two. Most importantly compared to the 01’ recession where unemployment peaked at 6.1%, the 09’ recession peaked at 9.6%. Logically because of the bigger damage done, it would take longer to get back to sustainable inflation.

Unemployment peaked at 6.1% in 2001 compared to 9.6% in 2010

Although a lot of market participants and financial market commentators are echoing about how the data dependent Fed is ignoring the data, we have to be sure we are focusing on the data they are looking at. With Fed Chair Yellen’s strong belief in the Phillips Curve, most likely she is focusing on unemployment and how the tight labor markets will force inflation to come back. This is what she is leading the Fed to stay on top of, the accelerating inflation that will come with rising wages. Market participants right now have only taken into account other economic data that has come out with pessimistic expectations. The most important thing to watch right now is unemployment and wage inflation. This is what it seems the Fed is basing their current views on.

Wage Inflation has a high correlation with Inflation

No comments:

Post a Comment